Student loans linked to greater harm for parents who borrow for their children than people who borrow for themselves

When people take out student loans for themselves, certain risks are involved. The debt can negatively affect a person's mental, emotional and even physical well-being. It can also harm a person's financial well-being.

But when taking out a student loan for one's child, the risk is even higher that the loan could be associated with lower financial well-being.

This is what economics scholar Charlene Kalenkoski and I found published in the Journal of Personal Finance. The study—which used a nationally representative federal dataset on household economics and decision-making—involved nearly 12,500 American adults ages 18 and over, with an average age of 48. It is not known whether the parents had taken out private or government loans for their children.

By lower financial well-being, we mean that these parents were more likely to report feeling as if they will never be able to have the things they want in life or that they are "just getting by financially." They also report feeling a lack of control over their financial situation. These statements are part of what the U.S. Consumer Financial Protection Bureau uses to measure financial well-being. Lower financial well-being decreases overall well-being.

Our findings remained consistent even after we took into account several other factors, such as the education levels of the parents, whether or not they work, how much they earn per year and how they spend their money. We also considered their financial literacy and their current financial strain.

The Consumer Financial Protection Bureau offers people a financial well-being score on a scale of 0 to 100. Taking out a student loan is associated with a lower financial well-being score for everyone, but our research found that it is associated with an even lower score when the loan is for the borrower's child. For instance, taking out a loan for oneself is likely to lower the score by 1.44 points, and taking out a student loan for one's spouse likely lowers the score by 1.37 points. However, taking out a student loan for one's child was likely to lower financial well-being scores by 1.88 points.

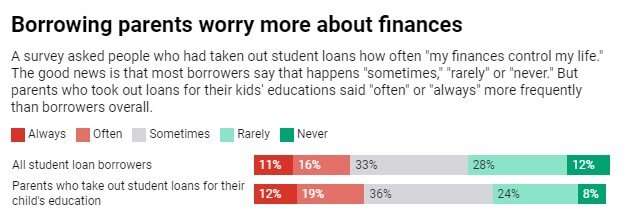

Most students rely on loans

In public policy discussions about people who take out student loans, it's not always clear whether the loan is for themselves or someone else, such as the borrower's spouse or child. Knowing this information provides insight into how student loan debt relates to the borrower's well-being if the loan is for their children.

In 2020, 64 percent of of college graduates financed their education via student loans—accumulating an average debt of US $29,927.

The combined amount of federal and private student loans—as well as the number of borrowers—continues to increase. The total amount of student loan debt reached $1.75 trillion as of Nov. 30, 2021, and the total number of borrowers stood at 47.9 million.

Negative effects on households

These student loan debts have adverse effects on individuals, households and the U.S. economy. Consequently, the federal government is considering federal student loan forgiveness. In a December 2021 letter, several Democratic lawmakers urged President Biden to extend the pause on student loan payments—which ends in January—and to act to cancel student debt.

The lawmakers call attention to "significant disparities" that contribute to the racial wealth gap. "Twenty years after starting college, the median Black borrower still owes 95 percent of their loans, compared to only 6 percent for the median white borrower," the lawmakers note, citing a 2019 Brandeis University study.

Studies have shown that student loan debt influences household decisions and outcomes. This includes delayed homeownership, lower likelihood of stock ownership, lower probability of life satisfaction and lower financial wellness compared with those without student loan debt.

Our study used a dataset for 2017. The long-term effects on parents' financial well-being after taking out loans for their children's college education are not known. Having datasets for longer periods of time would enable us to examine whether the loans cause lower financial well-being at different stages in parents' lives, such as when their children finally move out or when the parents retire.

Provided by The Conversation

This article is republished from The Conversation under a Creative Commons license. Read the original article.![]()