Potential debt problems more common among the educated, study suggests

(Phys.org)—Before the financial crash of 2008, it was highly educated Americans who were most likely to pile on unmanageable levels of debt, a new study suggests.

Overall, the percentage of Americans who were paying more than 40 percent of their income for debts like mortgages and credit card bills increased from about 17 percent in 1992 to 27 percent in 2008.

But college-educated people were more likely than those with high school or less education to be above this 40 percent threshold - considered to be a risky amount of debt for most households.

The association between more education and higher debt was true even after taking into account the fact that people with more education tend to have higher incomes.

In addition, people who reported being more optimistic about the future of the economy for the next five years were more likely to have a heavy debt burden, the study found.

"People who piled on debt may have been too optimistic about their economic future, but you can't blame that on a lack of education," said Sherman Hanna, co-author of the research and professor of consumer sciences at Ohio State University.

"People with college educations may have thought they were immune to any economic problems. But when people stop believing things might go bad, that's when they get in trouble."

Hanna and his colleagues also found that the debt crisis didn't just involve homeowners who took out bigger mortgages than they could afford. In fact, 35 percent of renters had a heavy debt burden in 2007, compared to 21 percent of homeowners.

Overall, Hanna said the research suggests that despite generally held assumptions, it wasn't just uneducated people, and not just homeowners, who precipitated the financial crisis by taking on too much debt.

"There wasn't just one group of Americans who were at fault," Hanna said.

"All types of households, renters and homeowners, educated and not, were taking on more of debt burden than they could bear. And lenders of all types - not just mortgage lenders - seemed to be taking more risks."

Hanna and his colleagues conducted two related studies, one appearing in the current issue of the International Journal of Consumer Studies and the other in the most recent Consumer Interests Annual.

In both studies, the researchers were interested in finding households that were paying more than 40 percent of their yearly income to pay off debt, including rent or mortgage, vehicle leases or loan payments, property taxes, credit cards, student loans and more. These were defined as households with a heavy debt burden.

"If more than 40 percent of your income is going toward debt, you're at a danger point, because if household income drops for any reason, it would be very difficult to keep up all your payments," Hanna said.

In both papers, the researchers looked at data from six rounds of the U.S. Survey of Consumer Finances held between 1992 and 2007, which included a total of 25,889 households. The SCF is sponsored by the Federal Reserve Board and asks detailed questions about families' balance sheets, pensions, income and demographic characteristics.

In the IJCS paper, the researchers found that college-educated people were more likely to have a heavy debt burden, even after taking into account not only income, but also income expectations, as well as their age and other characteristics that may influence debt burden.

"We just can't blame the lenders and say they were exploiting uneducated people who didn't know better. Many of those who got in over their heads were highly educated," Hanna said.

"There's plenty of blame to go around."

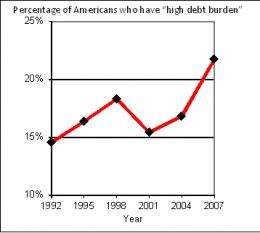

The percentage of households with a heavy debt burden increased from 1992 until 1998, but then dropped by 2001, when the United States went into a short recession, before rebounding again through 2007.

"Americans pulled back on their spending slightly during the slight recession of 2001, but after it was over debt levels continued to rise," Hanna said.

The Consumer Interests Annual paper found that the percentage of homeowners who had heavy debt burdens increased from about 15 percent in 1992 to 22 percent in 2007. However, the increase was even more dramatic for renters, going up from 20 percent to 35 percent during that same period.

"The percentage of renters who piled on debt really surprised me," Hanna said.

"It shows that the financial crisis wasn't all about housing speculation. There was too much debt in all parts of the economy."

More information:

www.blackwellpublishing.com/jo … al.asp?ref=1470-6423

www.consumerinterests.org/2012 … nference-papers.html

Provided by The Ohio State University